Doctors enter the workforce in a unique position; after years of school, residency, and student loans, they finally begin their practice and start bringing in real paychecks.

Due to their delayed start of their full wage-earning years, physicians and surgeons often get a late start on saving for retirement. Paying off student loans can also push retirement savings to the back burner. Nevertheless, your career as a medical professional provides you with the opportunity to not only catch up on retirement saving but to soar ahead (as long as you play your cards right).

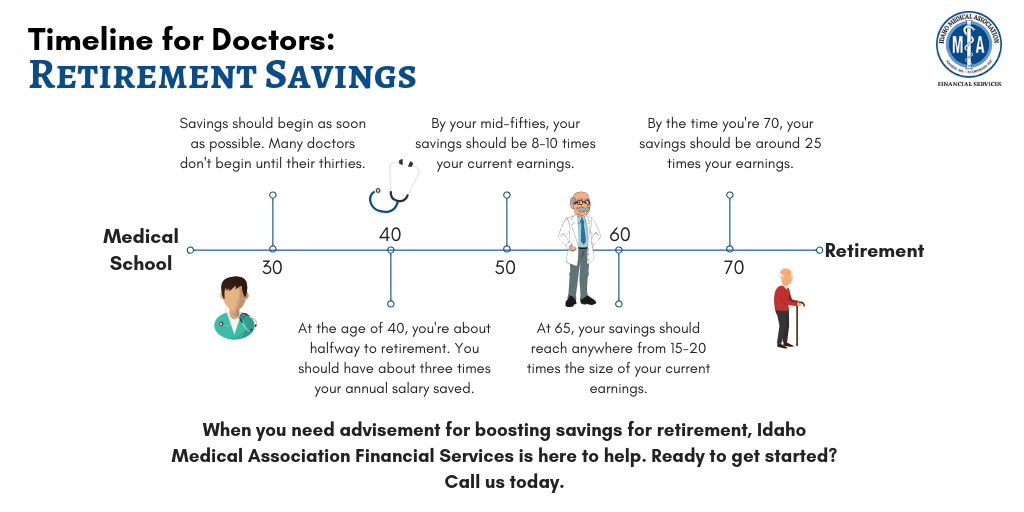

So where do you start? If you are a doctor in your 40’s, here some guidelines for how much you should save and how to get there.

Your Guide to Saving

When you reach the age of 40, you are likely about halfway to retirement. By this time, experts recommend that you have about three times your annual salary saved. So, if you are making $250,000 a year, you should have at least $750,000 in savings.

By your mid-fifties, that number should be 8-10 times your current earnings, and 15- 20 times by age 65. Don’t let these numbers scare you; remember that time and compound interest are on your side to help you reach these milestones. By achieving these goals, you are on your way to a retirement where you can continue your current lifestyle and spending habits.

Most people can achieve these goals by saving 15% of their income each year starting at age 25. However, at age 25, most physicians are still in the trenches of medical school and residencies. Thus, physicians should boost their savings rate during their high-income years. If you are further into your career and behind on retirement savings, you can adjust your savings strategy to reach your goals. In both situations, meeting with a financial expert at Idaho Medical Association Financial Services can help you create a plan catered to your unique circumstance.

A Couple Things to Keep In Mind

As you save, remember that where you are saving your money is just as important as how much you are saving. If you place your money in an account that accrues little to no interest, you will have to save much more to reach your retirement goals. For your money to grow faster and be protected against inflation, you must have a diversified retirement portfolio. Along with contributing to a 401(k) or Roth IRA, you should have a balance of investments with different levels of risk.

Remember, the amount you save will be based on the retirement lifestyle you would like to have. Some, who prefer a quiet retirement staying mostly at home, can get away with saving less than 15% annually. However, if you wish to travel extensively, pursue hobbies, donate to charity, or have other more expensive retirement goals, you should plan to save a little more. Consider your retirement goals as you evaluate your savings.

Get the Savings Help You Need

At Idaho Medical Association Financial Services, we specialize in creating retirement plans for medical professionals. Meet with a financial advisor to discuss your retirement goals and create a personalized plan for retirement that reflects your individual situation.