Often, people’s biggest fear when approaching retirement is that they will outlive their savings. This is a valid concern for many, considering that the average investor is far behind where they should be for a secure retirement. At Idaho Medical Association Financial Services, we offer financial planning for physicians and healthcare professionals in Canyon County and the surrounding areas. We help people ready themselves for the future every single day. One financial asset that many people have questions about are annuities.

What Do Annuities Do?

Annuities seek to alleviate that concern by providing a fixed amount of income over a specified time period, using a lump sum of cash. It is important to note that not all annuities are created equally; in fact, annuities run a very diverse spectrum ranging from fixed to variable annuities.

What Does This Mean For You, a Hopeful Retiree?

It means that before purchasing an annuity, you need to do your homework. It must first be understood that there are an enormous variety of annuities, each with their own advantages and disadvantages. Despite this diversity, there are a few traits annuities possess that are almost ubiquitous.

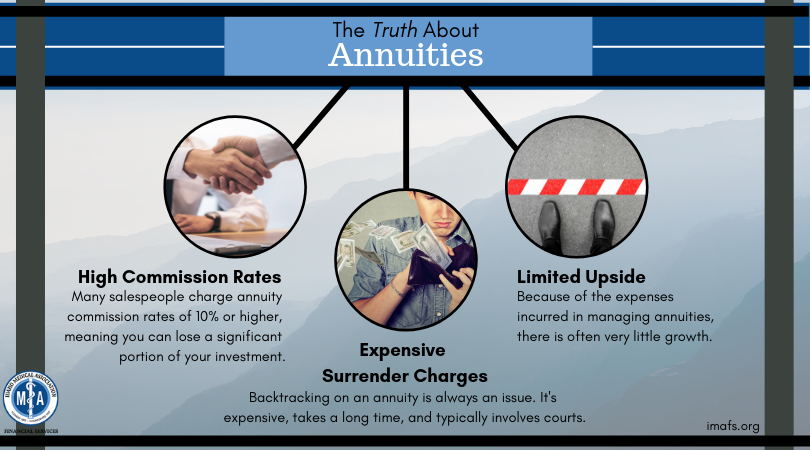

Annuities can be one of the highest-commissioned financial products that exist, which leads to a large group of very motivated annuity-selling financial advisors. The commissions on some annuities can be 10% or higher, which can be a powerful incentive for annuity salespersons to make sales. It might be worth noting that for a commissioned advisor, there is no obligation to put the interest of the client before that of the advisor. Often, this leads to a large gap between what the client needs, and what the commissioned advisor ends up selling them.

If you buy a $500,000 annuity that pays a 10% commission, that salesperson will walk out of the room $50,000 richer. Also, most annuities have surrender charge periods that can last 7-10 years or more. This won’t be a concern if you keep the annuity forever, but if you regret your purchase it becomes costly to backtrack.

In the end, the biggest downside to an annuity is the significantly limited upside. Just how limited may vary by annuity type, but all annuities incur a significant expense that pays for the insurance company to insure the value of your contract.

The Truth About Annuities

That said, annuities are not some terrible scam; their design can solve a number of critical financial problems for individuals, including superannuation (outliving your money) and creating some tax advantages when used correctly. However, in our opinion, most issues that annuities address can be solved more efficiently and inexpensively through other forms of financial planning.

In summary, while we do not believe that annuities are inherently a bad investment vehicle, we do acknowledge the many issues and inefficiencies surrounding them. That is why we at Idaho Medical Association Financial Services do not recommend or sell any type of annuity. Rather, we, as the best financial advisors for doctors in Canyon County, help our clients obtain security and growth using tried and true financial planning techniques such as low-cost efficient investing, global diversification, and individually-tailored portfolio allocations.

To learn more or set up a free consultation, visit our website at https://www.truenorthwealth.com/ or call (801)-274-1820.