Traditional, Roth, 401(k), IRA…each of these retirement account designations has its pros and cons. And when it comes to planning for retirement, you want to be sure you are getting the most out of your savings. The best choice for you will depend on your particular circumstances, and earnings.

Making the right choice is easy with help from Idaho Medical Association Financial Services, proud providers of retirement planning advice for healthcare professionals in Ada County, ID, and the surrounding region. Read on as we delve into the different types of retirement accounts.

Traditional VS. Roth: What’s the Difference?

Traditional and Roth accounts each provide effective ways to save for retirement. Both allow for tax free-growth while your money is in the account. The difference, however, lies in how and when that money is taxed.

When you contribute money to a Traditional IRA or 401(k), you are contributing money that has not yet been taxed. That money will be excluded from your taxable income for that year. However, you must be prepared to pay taxes on that money when you withdraw it.

On the other hand, Roth IRAs and 401(k)s are considered after-tax accounts, meaning that the money you contribute has already been taxed. When you withdraw money from a Roth account, it is tax-free.

Which Account is Right for Me?

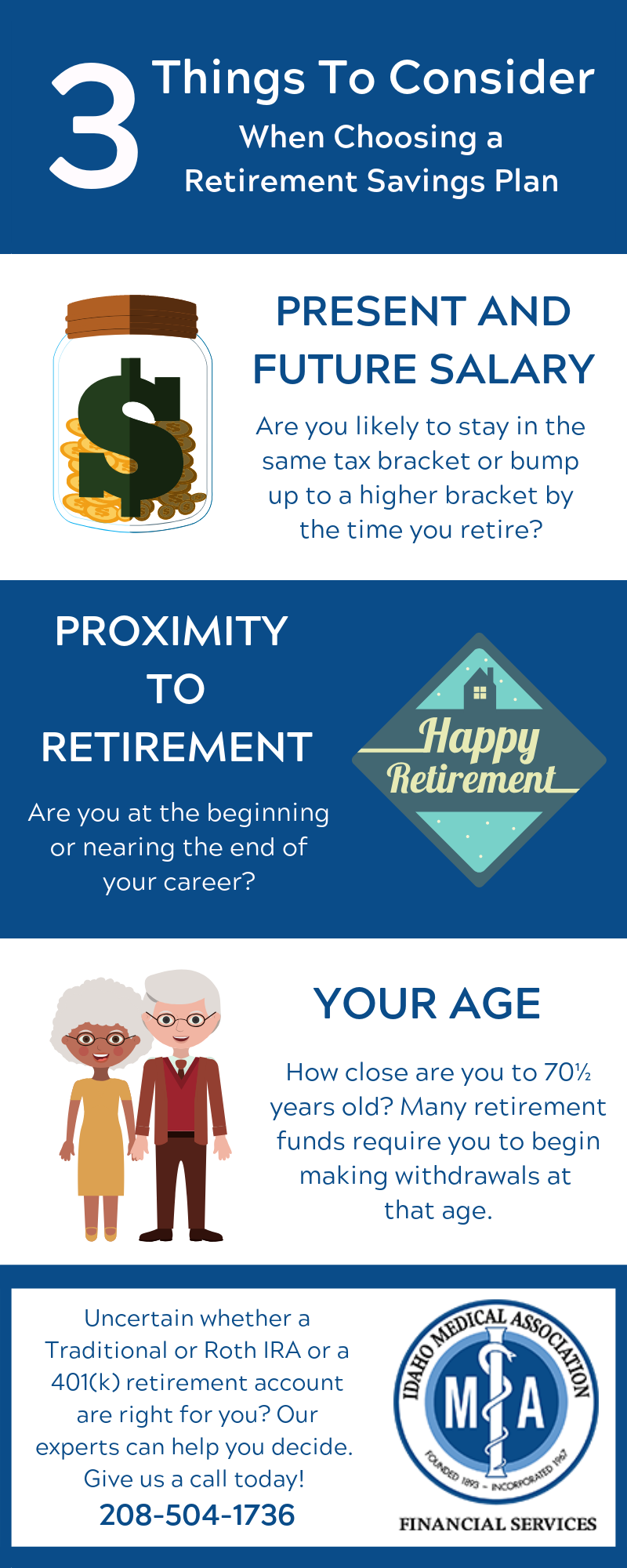

There are a few factors to consider when evaluating which retirement account type is better for your individual circumstance. We’ve outlined these factors in an infographic. Take a look, then continue to read as we expand upon each point below.

SALARY: If you expect your salary to stay the same or increase before you retire, a Roth account is the better investment choice. It is much more tax effective to pay taxes on your money while you are in a lower tax bracket. If your salary has grown by the time you retire, you will likely be taxed much more heavily.

PROXIMITY TO RETIREMENT: A Roth account is a superior choice for workers who are near the beginning of their career path. As a new worker, you still have years before retirement and so your salary is likely to increase. Additionally, your money will grow over time, and you will want to take advantage of the tax-free withdrawals that Roth accounts offer.

On the other hand, if you are in your peak earning years or expect to be in a lower tax bracket in retirement, you should consider making pre-tax contributions to a Traditional IRA or 401(k). The difference in tax brackets comes back to you as tax savings.

AGE: Additionally, Traditional IRAs and 401(k)s as well as Roth 401(k)s require you to begin withdrawing money at age 70½. These withdrawals are known as RMDs, or required minimum distributions. The only account type that does not have RMDs is a Roth IRA. If you are looking to avoid withdrawing the required amounts, talk with your advisor about the possibility of rolling your money over into a Roth IRA.

By using the proper retirement accounts at the proper times in your life, you can supercharge your retirement savings by making your financial situation more tax efficient. Each circumstance is different, so we encourage future retirees to consult with a financial advisor as they plan for their retirement.

For more information or to speak with a financial expert who handles retirement planning for doctors in Canyon County, ID, contact Idaho Medical Association Financial Services today.